Field workers, physicians, and the medical staff are rapidly adopting these solutions to access sensitive medical records and healthcare applications via wireless networks. On the basis of distribution channel, Geographically, in 2017, North America contributed the largest revenue to the mobile VPN market, and it is also anticipated to continue leading it during the forecast period. Within the continent, in 2017, the telecommunications sector registered the dominating revenue share in the North American market, due to the significant adoption of mobile devices here.

Get the Sample Copy of this Report @ https://www.psmarketresearch.com/market-analysis/mobile-virtual-private-network-products-market/report-sample

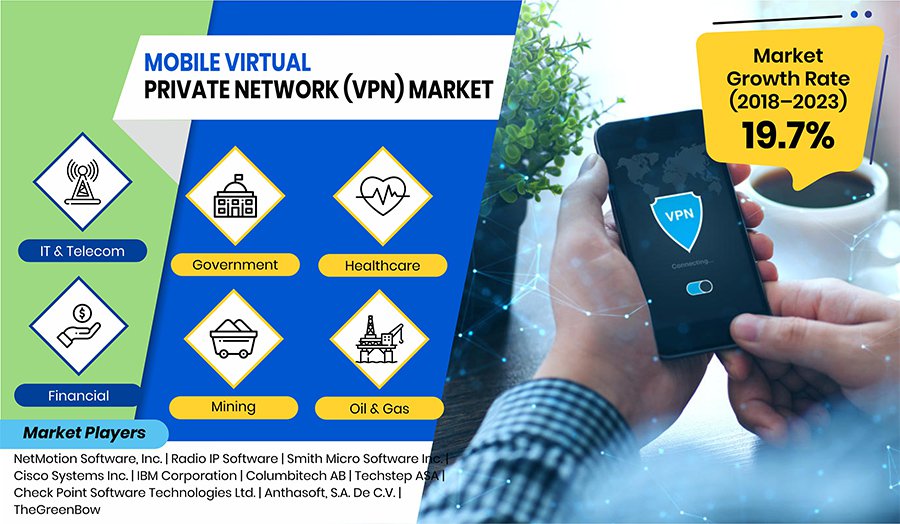

However, the Asia-Pacific region is predicted to witness the highest CAGR, of more than 30.0%, in the market during the forecast period.t of these, in 2017, the partners and distributors category contributed over 40.0% revenue to the market. The category is also predicted to dominate the market during the forecast period, as they offer better on-premises services compared to other suppliers. This is mainly attributed to the strong encryption algorithms of VPN with long-key strengths that help in securing confidential data at the time of transmission, which is critical for private and public enterprises.

Geographically, in 2017, North America contributed the largest revenue to the mobile VPN market, and it is also anticipated to continue leading it during the forecast period. Within the continent, in 2017, the telecommunications sector registered the dominating revenue share in the North American market, due to the significant adoption of mobile devices here. However, the Asia-Pacific region is predicted to witness the highest CAGR, of more than 30.0%, in the market during the forecast period.

Make Enquiry Before Purchase @ https://www.psmarketresearch.com/send-enquiry?enquiry-url=mobile-virtual-private-network-products-market

Nowadays, organizations prefer using centrally managed remote offices that help them provide a secure access to confidential data to their workforce at a low cost. Further, to reduce operational costs and maintain a local presence, enterprises are providing remote access to business-critical applications so that their employees can work from anywhere. Hence, mobile VPN is a vital solution for such enterprises, where employees have to access the company’s network via wireless devices.

It has been witnessed that the banking, financial services, and insurance sector spend a large portion of its revenue in mobile security services and products. Moreover, banks are aiming on protecting customers’ account details along with safeguarding the payment gateways. This has become especially important since the penetration of mobile devices in the bank-customer interaction environment. Thus, the surging need for the protection of data among companies is anticipated to offer huge growth opportunities to the mobile VPN market.

Hence, the increasing adoption of mobile VPN in various industries is expected to boost the growth potential for the market.