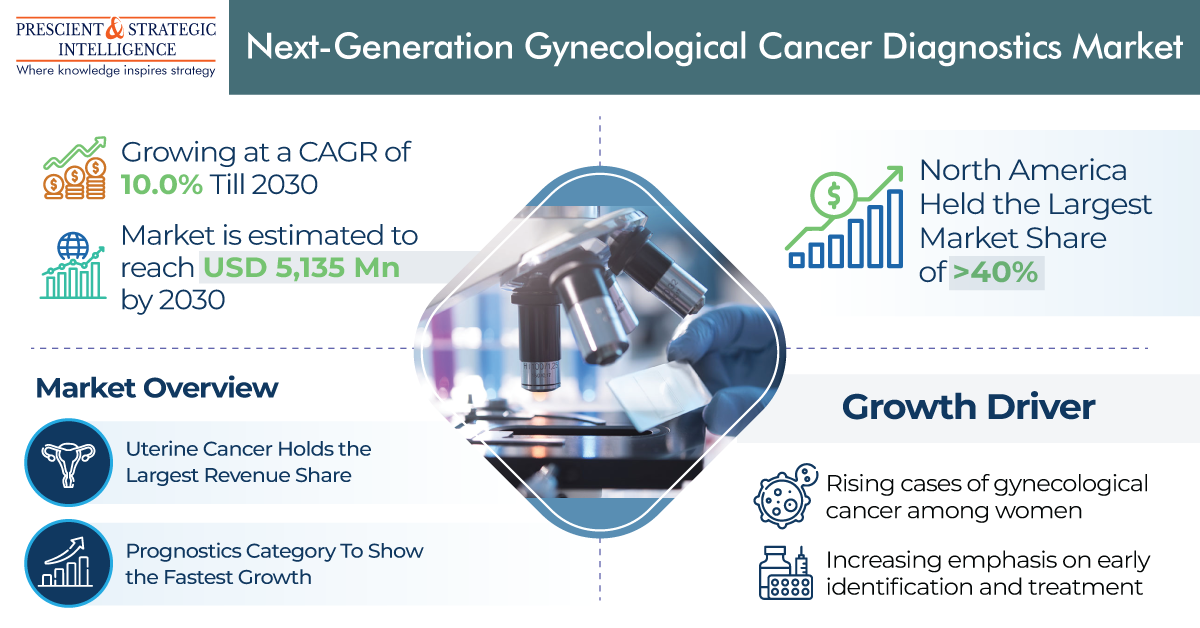

According to the latest market research study published by P&S Intelligence, the global next-generation gynecological cancer diagnostics market is undergoing a transformative shift, with its size projected to surge from USD 2.98 billion in 2024 to USD 6.09 billion by 2032, growing at a CAGR of 9.5%. This rapid expansion is fueled by the rising prevalence of gynecological malignancies, advancements in precision diagnostics, and increasing investment in women’s healthcare.

Download free Report Sample Now

Market Drivers: A Convergence of Healthcare Needs and

Innovation

- Rising

cancer incidence: Uterine, ovarian, and cervical cancers remain the

most common gynecological malignancies worldwide, intensifying the demand

for early and accurate diagnostics.

- Lifestyle-related

factors: Obesity, diabetes, menopause-related health issues, and

hormonal imbalances linked to diet are contributing to higher cancer risks

among women.

- Government

and regulatory support: Favorable policies, global awareness

campaigns, and healthcare investments are accelerating access to advanced

screening technologies.

- Technological

innovation: Next-generation sequencing (NGS), DNA microarrays, and

AI-powered multi-omics approaches are revolutionizing early cancer

detection and enabling personalized treatment strategies.

Emerging Trends: Multi-Omics and AI Integration

One of the most significant trends shaping this market is

the adoption of multi-omics approaches. These advanced methods identify unique

molecular signatures of gynecological cancers, allowing earlier and more

accurate diagnosis.

- In

India, the Indian Cancer Genome Atlas is pioneering national-level cancer

multi-omics mapping, strengthening research and precision medicine

capabilities.

- Companies

like Owkin are integrating AI and spatial omics to accelerate biomarker

discovery and improve clinical trial outcomes, exemplified by the MOSAIC

project.

- Regulatory

frameworks such as GDPR, OECD guidelines, and ICH standards are ensuring

data privacy, ethical practices, and global compliance in multi-omics

adoption.

Market Segmentation Highlights

- Technology:

NGS leads with a 65% market share in 2024, while DNA microarrays are

projected to grow at the fastest rate.

- Cancer

Type: Uterine cancer dominates with 60% share; however, cervical

cancer diagnostics is expected to grow at the highest CAGR due to rising

prevalence.

- End

User: Hospitals and ambulatory centers hold the largest share (75%),

while academic and research institutes will see the fastest growth.

Regional Growth Dynamics

- North

America remains the largest market (40% share), driven by strong

healthcare infrastructure, insurance coverage, and early adoption of

advanced diagnostics.

- Europe

is set to grow at the fastest CAGR, led by Germany, the U.K., and France,

supported by government programs and rapid technology adoption.

- Asia-Pacific

is emerging as a high-growth region, particularly in China and India,

where government-backed genomic projects and healthcare infrastructure

expansion are fueling demand.

Competitive Landscape

The market is consolidated, with key players including Roche,

Thermo Fisher Scientific, Illumina, Myriad Genetics, Hologic, and Agilent

Technologies, holding significant global presence through R&D investments

and strategic partnerships.

Recent Developments:

- June

2024: Thermo Fisher Scientific signed an MoU with National

University Hospital (NUH) and Mirxes to advance NGS genomic testing

tailored for Southeast Asian populations.

- March

2025: Agilent Technologies partnered with Hamamatsu, PathAI,

Proscia, and Visiopharm to launch an AI-powered end-to-end diagnostic

workflow for tissue analysis.

Looking Ahead