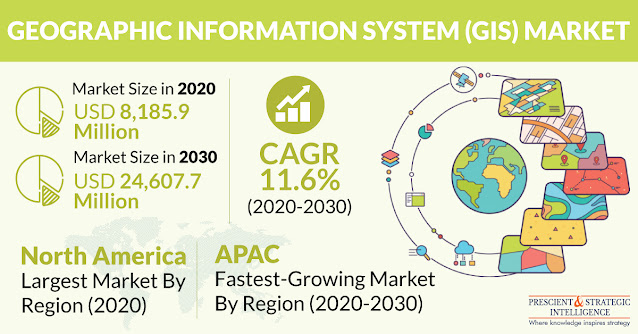

The global geographic information system (GIS) market value stood at $8,185.9 million in 2020, and it is predicted to exhibit a CAGR of 11.6% from 2020 to 2030 (forecast period). According to the estimates of the market research company, P&S Intelligence, the market will reach a value of $24,607.7 million by 2030.

The major factors fueling the expansion of the market are the surging investments being made in the GIS technology, abundant availability of cloud technology and spatial data, and burgeoning requirement for GIS solutions in the transportation sector. Geographically, the Asia-Pacific (APAC) region is predicted to be the fastest-growing region in the GIS market in the coming years.

This is ascribed to the growing urbanization rate and burgeoning need for geographic information systems in regional countries, such as India and China. Moreover, the governments of the regional countries have extensively used GIS solutions for various military applications in recent years in order to improve homeland security and infrastructure. The GIS market is highly consolidated in nature and the players are actively focusing on product launches and mergers and acquisitions in order to bolster their presence in the industry.

For example, Hexagon AB completed the acquisition of Immersal Oy, which is a provider of visual positioning and spatial mapping solutions which are used in augmented reality (AR) applications, in July 2021. With the help of this acquisition, the company started providing onsite deep insights, thereby improving the field of view with the aid of superimposed digital information.

Amongst these, the government sector held the largest share in the market in the past, as it extensively used GIS for several applications, such as information and data collection on natural calamities, urban and rural planning, and community planning. Besides developed nations, the governments of developing countries are also making huge investments in data-based and digital GIS technologies for rural and urban planning, optimal natural resource usage, and public health improvement.

Hence, the demand for GIS solutions will soar in the coming years, primarily because of their surging requirement in the transportation sector.

.jpg)