The video streaming market is witnessing the trend of the shift toward the OTT platform. It has been observed that in countries, such as the U.S., more than 150 million people have opted for OTT services, whereas more than 180 million people, use smart TVs. Further, people are opting for personalized content, which is pushing companies to offer high-margin visual entertainment by offering users bundled services. The rising popularity of OTT can be correlated to the rising consumer preference for specific content and better connection reliability offered by the service providers.

Get the Sample copy of this Report @ https://www.psmarketresearch.com/market-analysis/video-streaming-market/report-sample

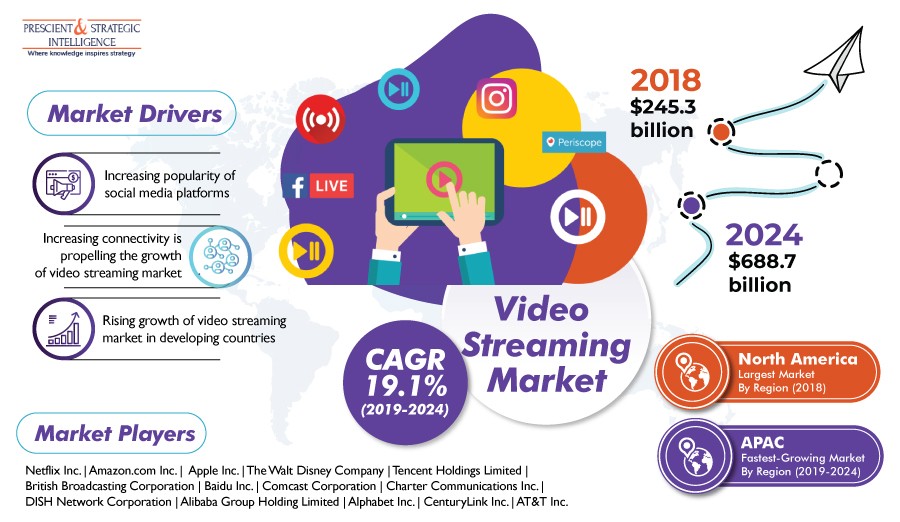

From amassing $245.3 billion in 2018, the global video streaming market is predicted to reach $688.7 billion by 2024, advancing at a 19.1% CAGR during the forecast period (2019–2024). The factors positively influencing the market growth are the rising popularity of video streaming in developing nations, growing internet connectivity, and the rising popularity of social media platforms. The accessing of the on-demand or live viewing of the content as per a consumer’s preference is termed as video streaming. This has been categorized into different services, including over-the-top (OTT), pay TV, and internet protocol TV (IPTV).

One of the major drivers of the video streaming market are the surging popularity of social media platforms, which can be credited to the improved access to the internet and connectivity. For instance, an explosive growth of 99% was exhibited by the video content on media platforms, such as YouTube in 2017. Further, these platforms are now increasingly being used as an advertisement revenue model for generating income. Based on this model, YouTube has generated the maximum revenue, which is closely followed by Facebook Inc.

Make Enquiry Before Purchase @ https://www.psmarketresearch.com/send-enquiry?enquiry-url=video-streaming-market

The categories of the video streaming market based on offering are service and solution. Between the two, in 2018, the higher revenue share of 94.6% was contributed by the solution category. Along with being extremely popular in the entertainment sector, video streaming solutions have become an important component for sales, marketing, business development, and corporate communications. This has resulted in their wide applications for personal as well as professional use. The solution category is further subcategorized into IPTV, OTT, and pay TV; among which the fastest growing subcategory is the OTT.